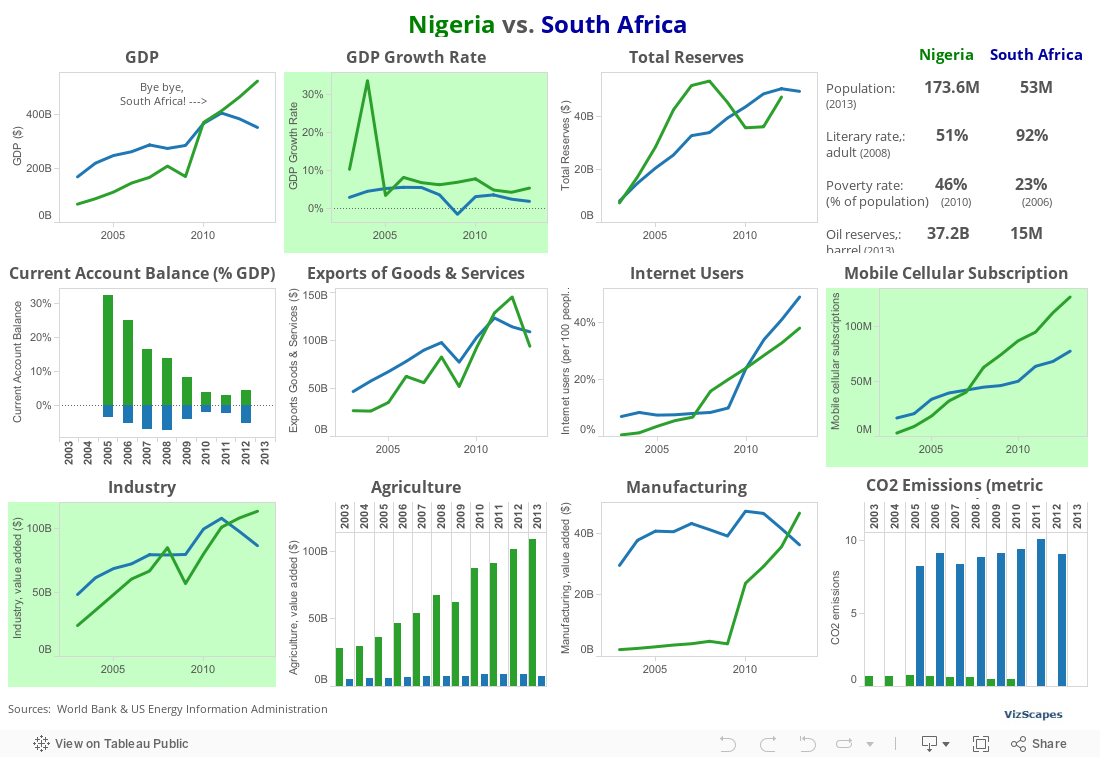

In April 2014, Nigeria surpassed South Africa as having the biggest economy in Africa. Nigeria’s Gross Domestic Product (GDP) was adjusted to $510 billion in 2013, 89% larger than previously estimated. This was because the economists adjusted how the country’s GDP was calculated, something they hadn’t done since 1990.

GDP adjustment is the process of replacing an old base year

with a more recent one which reflects the dynamic price structure and captures

economic growth. The IMF standard for GDP adjustment is every 5 years. But in Nigeria’s case, it took 24 years.

What had changed in the last 24 years was Nigeria’s fast economic expansion, changing from a financial base of crude oil to more diversified

activity including such vibrant sectors as manufacturing, agriculture,

financial services, mobile telephony and Nollywood. For example, the number of mobile phone

subscribers has leapt from a few hundred thousand customers to some 120M

today. The telecoms sector has jumped

from less than 1% to almost 9% of GDP.

Nollywood, which did not appear in 1990, is said to contribute 1.4% to

the GDP. More small and medium scale

enterprises (SMEs) have also been flourished. 1

Now that Nigeria’s GDP is larger than United Arab Emirates’

and South Africa becomes Africa’s Number Two, Nigeria is expected to continue

its 7% average annual growth, while South Africa’s economy would chug along

with 2% growth for next couple of years.

The reality is that Nigeria still has many problems to

overcome such as corruption, underdeveloped infrastructure, & large

poverty. However, Nigeria is a young

market and the opportunity is huge. "If

you're not in Nigeria, you're not in Africa," said Nigerian Finance Minister Ngozi Okonjo-Iweala.

_________________________

Note:

1 Mordi, Frederick, “Nigeria

overtakes rival South Africa”, African

Business, June 2014, pp. 74-75